Structure, Price and Manage any Type of Derivative or Structured Product

Numerix CrossAsset offers the industry’s most comprehensive derivatives pricing and risk management analytics library to empower users to structure, price and manage even the most complex derivatives.

In addition to the multitude of pricing models and its flexible architecture for defining bespoke deals, CrossAsset enables you to deploy a unified pricing and risk solution for all your derivative and fixed income positions across all trade types.

capabilities

Industry Leading Pricing and Risk analytics Library

The award-winning CrossAsset pricing and risk analytics library provides the industry’s most comprehensive cross-asset class library of market-standard models and advanced numerical methods. Whether you are valuing a vanilla option using one of our hundreds of pre-defined templates and closed-form pricers or creating a bespoke instrument using our unique payoff scripting language or Python, CrossAsset makes the pricing, valuation, and risk management of derivatives and structured product more efficient and accurate than ever.

Designed for Continually Evolving Capital Markets

The power of Numerix CrossAsset lies in the ability of end-users to perform pricing and risk calculations on any derivative at runtime, without requiring any recompilation or redistribution of the CrossAsset library. This "data-driven" approach to pricing allows the CrossAsset library to stay relevant in the quickly changing field of derivative pricing.

Recognized Leader in Pricing and Risk Analytics for Exotic Derivatives and Complex Hybrid Derivatives

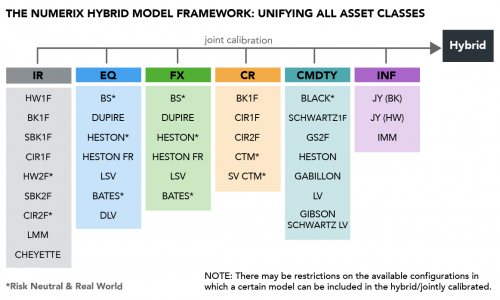

Numerix's hybrid model framework produces accurate valuations for instruments consisting of multiple underlyings through joint calibration and incorporating multiple stochastic processes.

Benefits & Features

Fair Pricing & Transparency: Pre/post-trade pricing of financial derivatives

Comprehensive Model Coverage: Richest set of models and full transparency with deep insights into calculations

Counterparty Risk Analytics: Cutting edge CVA, DVA, FVA, PFE and other exposure measures

Consistent & Accurate Risk Outputs: Accurate risk numbers across all asset classes including hard to price exotic derivatives

Scenario Analysis: Bump & twist any risk factor

Cutting-Edge Multi-Curve Framework: Flexible multi-curve, multi-currency pricing with sophisticated global solving

Full Support for Risk-Free Rates: Complete coverage for all global Alternative Reference Rates (RFRs)

Additional Resources

Product Collateral

Numerix Models and Instruments Library: Access Models for All Major Assets Classes,...

Product Collateral

Numerix CrossAsset Fact Sheet

Product

CrossAsset ESG: Risk Neutral and Real World Economic Scenarios

Product

CrossAsset SDK: Quick Integration Into Any Proprietary or Third-Party Systems

Product

CrossAsset XL: Rapidly Structure, Price and Manage Risk for Any Derivative

Navigating the LIBOR Transition with CrossAsset

Product

Structure and Price Any Type of Derivative or Structured Product